At a petrol pump in Jaipur, the queue begins before sunrise. A delivery driver leans against his scooter, checking his phone for updates on fuel prices. Behind him, a shop owner counts cash twice before stepping forward fuel is already eating into his margins.

A rumor moves faster than the line: supplies might tighten.

The pump attendant shakes his head. “Stock is coming,” he says, almost rehearsed. But the unease lingers. Not because fuel has run out but because the world, suddenly, feels closer than it should.

The war in West Asia geographically distant but economically intimate has forced India into a familiar balancing act: protect its growth story while ensuring ordinary citizens don’t absorb the shock. Prime Minister Narendra Modi has publicly assured that the government is working to ensure “the burden does not fall on common people,” even as global shortages of fuel, gas, and essential commodities ripple across economies.

This moment matters because it reveals a deeper truth about modern India: its economic rise is increasingly tied to global stability and its political leadership is now judged on how well it can insulate 1.4 billion people from forces beyond its control.

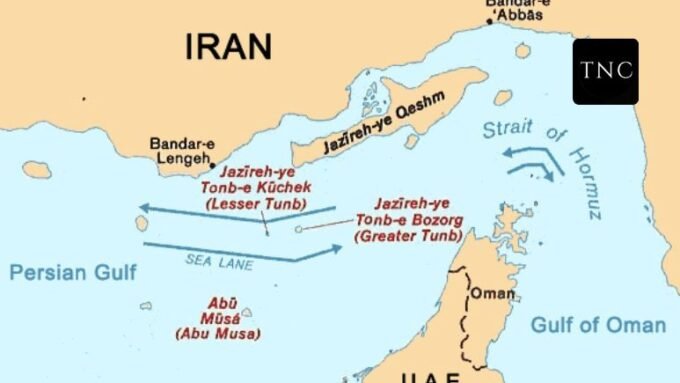

India’s vulnerability begins with energy. Nearly two-thirds of its oil comes from West Asia, making every disruption in the region a direct threat to domestic inflation and growth. When conflict disrupts shipping lanes or drives up crude prices, the impact travels quickly from refineries to transport costs to household budgets.

The government’s response has been multi-layered and strategic.

First, control the narrative. Officials have repeatedly emphasized that fuel, LPG, and essential goods remain adequately stocked. This is not just reassurance; its economic policy. Panic buying can create shortages faster than war.

Second, tighten coordination. The Centre has urged states to act as “Team India,” focusing on preventing hoarding, stabilizing supply chains, and maintaining public confidence.

Third, deploy institutional response mechanisms. Seven empowered groups have been formed to monitor everything from fuel supplies to inflation risks mirroring the crisis management model used during Covid.

But beneath the coordination lies a harder reality: insulation has limits.

Recent data shows that India’s private sector growth has already slowed to a three-year low, with rising input costs driven by energy and commodity price shocks. Oil price spikes reportedly up to 40% in some scenarios feed directly into inflation, squeezing businesses and consumers alike.

And yet, the government continues to project confidence. Growth is still expected to hover around 7% or higher, supported by infrastructure investments, domestic demand, and policy interventions.

This dual narrative resilience versus risk is not contradictory. It is the defining tension of India’s current economic moment.

India is no longer a fragile economy reacting to crises. It is a large, interconnected system trying to manage them.

The line at the petrol pump may move. Prices may stabilize. Supplies may hold.

But the bigger shift is already underway.

India’s growth story is no longer just about what happens within its borders it’s about how well it can absorb shocks from beyond them. The promise that the “burden won’t fall on common people” is not just political messaging.

It is the hardest test of a rising economy:

Can it grow globally without making its citizens pay locally?

Also Read / India’s Energy Gamble: Racing Against a Chokepoint Crisis.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment